It used to be that companies went public after achieving a modicum of success. There were business models, calculations, and plans, all based on real results and proven success.

Now it's all about potential.

There are still plans and projections, but proven success has been hard to come by.

Remember, Pets.com had a plan. It was going to change the way we took care of our animal buddies. Only, it didn't. And now it's gone.

Kozmo.com was supposed to be a messenger service that embodied online delivery. It's gone, too.

Epidemic.com? Gone. WebVan? Gone. Lastminut.com? Gone. Dr. Koop? Gone.

Despite the media hoopla at the time, investors were ultimately left high and dry. And now it could happen again...

Twitter, the micro-blogging social media darling, has finally filed for its much ballyhooed IPO. And the valuations being assigned to it range from $12 billion to as much as $25 billion.

That's asinine for a company that hasn't shown any profit potential.

Twitter Inc. may make a fine trading instrument, as long as the party continues. But as an investment?

You can #countmeout...

You Need Widespread Adoption to SucceedCelebrities like Alec Baldwin, Ashton Kutcher, Sinéad O'Connor, and Jennifer Love Hewitt, who helped put Twitter on the map, are leaving because of their increasing unwillingness to deal with the venomous responses and insults left on their account pages.

I can't say I blame them. The level of vitriol piled on by those who hide behind the veil of Internet anonymity is staggering.

That's going to cut down on the need for "compelling" content - assuming you find that kind of thing compelling. I don't.

Twitter has throttled its API. What this means, according to Wired.com's Marcus Wohlson, is that the company is willing to "alienate some of its most impassioned users to consolidate control" by substantially restricting third parties from developing Twitter applications.

I can't say I disagree. The key to any company is widespread adoption from both users and vendors alike. Look at how rapidly Android has grown. It wasn't the platform that changed but the apps that made this possible. Apple Inc. (Nasdaq: AAPL) and Microsoft Corporation (Nasdaq: MSFT) are struggling, and could be headed the way of BlackBerry Ltd. (Nasdaq: BBRY)... which failed because the number of quality apps for it stunk.

And, finally...

Twitter Is Not FacebookThat's heresy, according to the technorati who are quick to compare the two companies now in the same breathless terms they used back in the dot.bomb heyday. Never mind that's what they said about AOL Inc. (NYSE: AOL), too.

Unfortunately, the market doesn't seem willing to reinforce the lesson. There are huge amounts of capital chasing anything that's got even the remotest hint of promise at a time when investors are desperate for returns.

Despite a badly botched IPO, Facebook Inc. (Nasdaq: FB) is now heralded as a success, and investors who were swearing off stocks for having bought it are now confusing Bernanke's stimulus-altered reality with genius. So they're comparing the two companies.

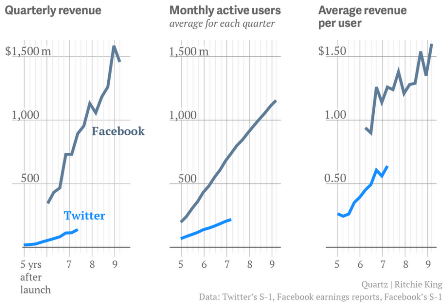

The problem is that Twitter is not even remotely Facebook. It's not even remotely the size Facebook was at this stage of its development. More to the point, it's not growing nearly as fast.

Ritchie King makes this abundantly clear in this chart from Quartz below.

And that's what really breaks it for me: the numbers.

According to Wikipedia, September 2011 saw Twitter with 100 million active users. By December 18, 2012 - a year later - there were 200 million monthly active users. By the time the company filed its S-1, that rapid growth had slowed down to only 218 million active users or a 9% year-over-year growth rate... down from 100% the year before.

Ad rates per user fell 46% on a basis in June, according to the company. What this means, according to Teirnan Ray of Barron's, is that, while the "number of ad slots the company had available to sell expanded greatly," that "didn't lead to a proportionate increase in ad buying."

Since inception, the company has racked up nearly $500 million of accumulated deficit. Losses have widened 41% to $69.3 million, which puts Twitter on pace to lose $138.6 million by year end.

Facebook trades roughly at 20 times sales, while LinkedIn Corp. (NYSE: LNKD) is at 21. An IPO at $12.8 billion would represent approximately 28.6 times earnings, according to Bloomberg. Goodwill and unproven potential evidently counts for a lot these days.

The Bottom LineIf you're thinking about investing in Twitter's IPO, you have to ask yourself: Do you really want to spend your hard-earned money on an IPO where you are, quite literally, the last in line on the profit train?

I don't.

The IPO process is a rigged game where the founders, early investors, and investment bankers make out like bandits. As a retail buyer, you really are the last in line.

Twitter has the same problem that any social media company has... it's got to convert eyeballs into paying customers. That may never happen because...

#Thenextbestthingisonlyaclickaway...

No comments:

Post a Comment