Tuesday, April 30, 2013

Why Meritor's Shares Popped

Although we don't believe in timing the market or panicking over market movements, we do like to keep an eye on big changes -- just in case they're material to our investing thesis.

What: Shares of automotive equipment supplier Meritor (NYSE: MTOR ) jumped 23% today after the company released earnings.

So what: Sales dropped 22% to $908 million and the company reported a net loss of $4 million, or $0.04 per share. Revenue fell short of estimates but investors are clinging to adjusted earnings per share of $0.06, which came in a penny ahead of expectations.

Now what: Investors are betting on a big turnaround for Meritor and management is hoping for adjusted earnings of $0.25-$0.35 per share this year. I just don't like the trends we're seeing right now from a revenue perspective. I'm going to leave this move alone today and wait for more sound fundamentals before looking at the stock again.

Interested in more info on Meritor? Add it to your watchlist by clicking here.

More Expert Advice from The Motley Fool

The Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock in our brand-new free report: "The Motley Fool's Top Stock for 2013." I invite you to take a copy, free for a limited time. Just click here to access the report and find out the name of this under-the-radar company.

Bank of America’s Legal Battle Heats Up, Sending Shares Lower

Shares of Bank of America (NYSE: BAC ) are lower today after mixed news from its ongoing legal battles continues to trickle in. Roughly halfway through the trading session, the nation's second largest lender is down by $0.07, or 0.53%.

In a decision issued yesterday, a judge in New York denied a motion by bond insurer MBIA (NYSE: MBI ) which would have held Bank of America wholly liable for all of Countrywide Financial's pre-crisis misdeeds. While the bank has verbally committed to assuming Countrywide's liabilities -- its CEO Brian Moynihan said in 2010 that, "At the end of the day, we'll pay for the things Countrywide did" -- that's a far cry from being legally obligated to.

The issue, known as "successor liability," has been used as a bargaining chip by Bank of America in negotiations with various parties throughout a multitude of settlement discussions -- most importantly an $8.5 billion agreement with institutional investors in mortgage bonds backed by Countrywide-issued home loans. The fear was that an adverse ruling in the MBIA case could therefore influence other legal proceedings and settlement discussions.

Notably, the judge also denied Bank of America's motion to have the issue decided wholly in its favor, leaving the question one for a jury to decide.

Down the street, a federal judge expressed skepticism over the Justice Department's use of a rarely applied law to sue Bank of America over the sale of toxic mortgages to Fannie Mae and Freddie Mac in the lead up to the financial crisis. The lawsuit seeks $1 billion in damages and alleges that the bank engaged in a scheme, known as "the Hustle," to defraud the government-sponsored agencies in order to boost revenues in 2007 and 2008.

The judge was concerned specifically about the Justice Department's reliance on the Financial Institutional Reform, Recovery and Enforcement Act of 1989, which was passed to combat abuses committed throughout the savings and loan crisis. The law entitles the government to seek damages from anyone who commits a fraud that affects a federally insured financial institution.

In this case, however, neither Fannie Mae nor Freddie Mac was formally insured by the federal government at the time of the alleged misdeeds. Consequently, the Justice Department is arguing that community banks -- which are insured by the FDIC and that owned preferred shares of the GSEs -- were the victims. The judge said he was "troubled" by this application of the law and said he'd issue a final ruling on the matter on May 13.

Make no mistake about it, how these legal cases turn out is critical to the performance of Bank of America's shares. If you want to learn more about this, I urge you to read this series on the bank's legal woes. And if you're looking to learn more about Bank of America in general, check out our comprehensive, in-depth report on the lender by clicking here now.

How You Can Profit From China's $9 Billion Gaming Market

Over the past decade, China's gaming market has exploded. Recognizing that games could be a powerful cultural tool to teach its citizens about history and culture, the gaming market grew from less than $160 million in 2003 to a $9 billion market in 2012. Of course, the biggest benefactors have been domestic gaming giants, but there are some who have profited more than others.

Two companies that seem on an unstoppable path of profits are Giant Interactive (NYSE: GA ) and NetEase (NASDAQ: NTES ) . Meanwhile, Shanda Games (NASDAQ: GAME ) and Perfect World (NASDAQ: PWRD ) haven't done as well.

In the video below, Fool contributor Kevin Chen outlines how you should think about China's gaming market. Through learning about these companies' successes and failures, you'll get a better understanding for why licensing agreements won't work -- even if it is with Activision Blizzard (NASDAQ: ATVI ) -- and how you can profit from the Chinese government's policies. To learn more, watch the video below.

While investors have gotten rich by investing in China's gaming market, you don't have to limit yourself to just these companies. When you really think about it, much of our digital and technological lives are almost entirely shaped and molded by just a handful of companies. Find out "Who Will Win the War Between the 5 Biggest Tech Stocks?" in The Motley Fool's latest free report, which details the knock-down, drag-out battle being waged by the five kings of tech. Click here to keep reading.

Monday, April 29, 2013

Archer Daniels Midland: Third Time Pays for All

Believing the third time is the charm, grain processor Archer Daniels Midland (NYSE: ADM ) submitted its third bid for GrainCorp and at least didn't have it rejected like the other two. Now it can go on and start its due diligence process, after which it can formally submit a takeover offer.

The acquisition saga began last October, after ADM took a nearly 15% stake in the Australian grains receiving and storage specialist and then decided it wanted to own the whole thing after all. It bid $12.13 per share cash for it, but it was promptly rejected. ADM then increased its position in GrainCorp to almost 20% and upped the amount it would pay to takeover the company to $12.73 but was again rejected as still undervaluing its operations despite the premium being offered.

ADM decided to let management and investors stew over the lost opportunity and let the matter lie for a few months until last week, when it announced it was sweetening the pot yet again in what perhaps could be seen as a best and final offer. Although ADM still values GrainCorp at $2.9 billion, it's now putting some gristle on the bone it's throwing investors, adding in $1 per share in dividends, which raises the total bid to $13.56, or $3.5 billion.

The grains processor is looking to GrainCorp to give it a launching paid into Asian markets, and it noted there is little geographic overlap between the two. More than half of ADM's revenues are generated in the U.S., and another fifth comes from France and Germany.

ADM needs to bolster its presence in the Orient, where traders estimate that it supplies 12% to 17% of the country's soybean imports. GrainCorp handles up to 60% of the region's wheat, barley, canola, chickpea, and sorghum crops through East Coast-based bulk grain elevators, where seven of its eight elevators are located.

Rivals such as Bunge (NYSE: BG ) already have a larger presence already in the region, with Bunge generating 18% of its $62.9 billion in revenues from Asia. It derives less than a third from the U.S., thus spreading out its geographic risk better.

In February, ADM reported second-quarter earnings that continued to be weighed down by its heavy reliance on ethanol production, which have been producing persistent, negative margins. So although the cooling-off period between its last offer and the one it made last week gave GrainCorp some time to think the merger over, it also proved to ADM that it needs this deal just as much.

If you'd like to juice up your own portfolio with more dividends, The Motley Fool has compiled a special free report outlining our nine top dependable dividend-paying stocks. It's called "Secure Your Future With 9 Rock-Solid Dividend Stocks." You can access your copy today at no cost! Just click here.

Why Century Aluminum's Shares Jumped

Although we don't believe in timing the market or panicking over market movements, we do like to keep an eye on big changes -- just in case they're material to our investing thesis.

What: Shares of Century Aluminum (NASDAQ: CENX ) jumped 13% today after the company announced an acquisition.

So what: The company is buying the Sebree aluminum smelter for about $61 million in cash from a subsidiary of Rio Tinto Alcan. Century will assume $71 million in working capital and won't be liable for historical environmental liabilities at the plant.

Now what: This is an extremely low-cost acquisition and will add about 205,000 metric tons of aluminum capacity to the company. Management didn't make any predictions as to the impact on revenue or earnings but the assumed working capital makes this a very low risk acquisition. If Century Aluminum can live up to expectations over the next year I think the stock has room to run higher, fueled by this latest acquisition.

Interested in more info on Century Aluminum? Add it to your watchlist by clicking here.

Why Balfour Beatty, Greggs, and Nanoco Should Lag the FTSE 100 Today

LONDON -- The FTSE 100 (FTSEINDICES: ^FTSE ) isn't doing much today. The index of top U.K. shares is up a meager 12 points, or 0.19%, as of 9:25 a.m. EDT. Recent economic news has failed to clarify the medium-term outlook, and many are waiting for the next moves from central banks -- although the formation of a government in Italy has at least eliminated one bit of uncertainty.

News for companies is not all good today, either, with profit warnings taking some of the shine off recent upbeat earnings reports. Here are three companies slipping today.

Balfour Beatty

Balfour Beatty shares have slumped 10.2% this morning after the construction company issued its second profit warning in six months. The firm's U.K. construction business is now "expected to deliver significantly lower profits from operations for 2013 than management's expectations at the time of the full-year results announcement in March," as tough market conditions over the second half of 2012 are continuing.

Profit from U.K. construction is likely to be reduced by about 50 million pounds, or 20%, from previous expectations, with an additional profit deterioration of 10 million pounds expected from the firm's German rail operations.

Greggs

Another profit warning, this time from Greggs, sent shares in the high-street baker tumbling by 7.5%. Blaming adverse weather in January and March, Greggs revealed a 4.4% fall in like-for-like sales, although there are signs that the drop has been leveling off in recent weeks.

The company said, "We do not expect a significant improvement in the difficult underlying market conditions in the short term," and that profit should be "slightly below the lower end of the range of market expectations." But even taking that into account, the year-end prospective P/E looks likely to be around 11.5, and if it's maintained, there's a dividend yield of around 4.5% forecast.

Nanoco (LSE: NANO )

Quantum dot developer Nanoco has seen its shares falter a little, down 2% after the firm announced that nonexecutive chairman Peter Rowley is to step down from the position after serving seven years in the chair. Rowley will become a nonexecutive director, with current nonexecutive director Anthony Clinch taking over the chairman role.

Nanoco's shareholders have been rewarded nicely over the past 12 months, with the price more than doubling -- though earlier in 2013 the shares were changing hands for as much as 199 pence.

Finally, reliable dividends can more than compensate for the day-to-day ups and downs of share prices. So how about a company that's offering a 5.7% yield and could be set for some nice share-price appreciation, too? It's the subject of our brand-new report "The Motley Fool's Top Income Share For 2013," which you can get completely free of charge -- but it will only be available for a limited period, so click here to get your copy today.

Will Eli Lilly's Big Bets Pay Off?

Tomorrow, Eli Lilly (NYSE: LLY ) will release its latest quarterly results. The key to making smart investment decisions on stocks reporting earnings is to anticipate how they'll do before they announce results, leaving you fully prepared to respond quickly to whatever inevitable surprises arise. That way, you'll be less likely to make an uninformed kneejerk reaction to news that turns out to be exactly the wrong move.

The pharmaceutical industry has a lot of opportunities for growth right now, and Eli Lilly has done its best to claim its share of those opportunities. But Lilly faces a tough road in building up its pipeline to offset the impact of expiring patent protection on some of its blockbuster drugs. Let's take an early look at what's been happening with Eli Lilly over the past quarter and what we're likely to see in its quarterly report.

Stats on Eli Lilly

| Analyst EPS Estimate | $1.05 |

| Change From Year-Ago EPS | 14% |

| Revenue Estimate | $5.66 billion |

| Change From Year-Ago Revenue | 1.1% |

| Earnings Beats in Past 4 Quarters | 3 |

Source: Yahoo! Finance.

Will Lilly deliver healthy results this quarter?

In recent months, analysts have gotten more optimistic about Lilly's earnings prospects. They've made a $0.07 per share increase both to their first-quarter and full-year 2013 estimates, helping to send the stock to about a 10% gain since mid-January.

The toughest obstacle for big pharma lately has been the wave of patent expirations hitting the industry. Pfizer (NYSE: PFE ) has had to deal with the loss of Lipitor, which produced more than $130 billion in lifetime sales, as well as several other important drugs in its lineup. Fellow giant Merck (NYSE: MRK ) had to lower its 2013 forecast when its Singulair patent protection expired. Yet even with the whole industry facing the patent cliff, Lilly is having to deal with expiring patents on drug after drug, including Zyprexa in 2011 and Cymbalta at the end of this year, and its pipeline hasn't delivered on its full promise to replace those lost sales.

To address those concerns, Lilly has turned to oncology and diabetes treatments, which make up the vast majority of its stable of clinical-stage drugs. Just last week, the company announced favorable results on phase 3 trials of its dulaglutide treatment for type 2 diabetes, including signs of superiority over Sanofi's (NYSE: SNY ) Lantus. In addition, Lilly is still seeking to address Alzheimer's disease, having made a deal with Germany's Siemens (NYSE: SI ) to obtain imaging tracers that could help it develop treatments for the disease.

Still, Lilly has had to take tough measures in light of its patent cliff. Earlier this month, the company said it would have to restructure its sales force, with job cuts expected by July 1. The restructuring could result in a net job loss of roughly 700 workers as the company strives to contain costs.

In Lilly's report, watch closely for signs of how well its cost-containment measures are doing at preserving profits. Lilly needs to make the most of Cymbalta before it loses patent protection, and shoring up its finances to withstand the coming hit is essential.

With key drugs poised to lose patent protection this year, is Eli Lilly a dividend stock headed nowhere fast? In a new premium report, The Motley Fool's senior pharmaceuticals analyst breaks down all of Lilly's moving parts, including an in-depth analysis of the company's must-know opportunities and reasons to buy and sell today. To find out more click here to claim your copy today.

Click here to add Eli Lilly to My Watchlist, which can find all of our Foolish analysis on it and all your other stocks.

Sunday, April 28, 2013

3 Reasons Tesla Stock Will Hit a New High in 2013

Tesla Motors (NASDAQ: TSLA ) continues to prove its critics wrong, one milestone after another. Last year, the company delivered its all-electric Model S ahead of schedule, won Motor Trend's 2013 Car of the Year, ramped up production, and launched a U.S. Supercharger Network. Tesla rode this momentum into 2013, and now expects to post its first profit when the company reports earnings on May 8. Tesla stock is up more than 50% year to date because of all the upbeat news. However, with Tesla's stock trading around $50 a share, some investors worry that it's too late to get in on the action.

Here are three reasons why Tesla stock should move higher from here.

1. Tesla is a disruptive force in the auto industry

Tesla Motors is a disruptive innovator that's bent on forever changing not only the way we drive, but also the way we buy cars. Unlike traditional car manufacturers, such as Ford or General Motors, Tesla doesn't sell its cars through franchised dealerships. Instead, the company's retail strategy relies on mall stores located in high foot-traffic areas.

Not surprisingly, pushing for change in an industry that's operated the same way for more than 100 years hasn't been easy for Tesla. Auto-dealer groups in states such as New York and Massachusetts brought lawsuits against Tesla, saying that it violated state franchise laws. Tesla fought back, and won.

As it stands, Tesla has won the right to operate its manufacturer-owned stores in more than eight U.S. states. Tesla stock should get a meaningful boost if the company can win over the state of Texas in the coming months.

2. The stock's current valuation is deceiving

There's no shortage of investors betting against the company. In fact, as of this writing, Tesla stock has a short interest of more than 42%. For comparison, less than 2% of Ford's stock is currently sold short. Meanwhile, even GM's short float of 12% looks good next to Tesla stock. Nevertheless, this could end up working to Tesla's advantage in the case of a short squeeze.

Additionally, many would-be Tesla investors argue that the stock is overvalued compared to other automakers, such as Ford or General Motors. This isn't without merit if you're simply looking at the numbers. However, as an upstart growth stock, I'd be worried if Tesla's valuation were comparable to these traditional auto companies.

It's a mistake to value Tesla using the short-term benchmarks reserved for established auto companies. Conversely, investors who are willing to take a long-term approach to valuing Tesla stock will have the most to gain when the naysayers buy in down the road -- particularly, if Musk delivers on his promise of making Tesla the greatest automaker of the 21st century.

The lesson here is: Don't judge a stock by its valuation alone. Finding winning investments is about more than numbers. It is equally important to understand the business behind those numbers. In Tesla's case, I think it is one of the most misunderstood stocks on the Nasdaq. However, this will change in time as the company continues to exceed expectations, and that's when longtime shareholders will be rewarded.

3. Visionary leadership at its best

Thanks to Apple's Steve Jobs, the world has seen what visionary leadership can do for a company. Tesla's CEO Elon Musk is no exception. Musk has a proven track record of success, including co-founding PayPal, which, in 2002, was purchased by eBay for a cool $1.5 billion. More recently, Musk made history when his company SpaceX launched the first commercial spacecraft to reach the International Space Station. Not to mention, SpaceX locked down a $1.6 billion contract with NASA, in the process.

While transforming U.S. space travel is certainly remarkable, what Musk has achieved with Tesla is equally impressive. With Musk at the helm, Tesla has overcome insurmountable odds as a start-up electric car company trying to succeed in an industry where economies of scale favor the traditional automakers. If history is any indication, Musk knows how to build and run a successful business.

It isn't everyday that you find CEOs, such as Jobs or Musk, with the vision to revolutionize entire industries. For this reason, I plan to own Tesla stock well into the future, and certainly for as long as Musk remains at the top. Patient investors should buy Tesla stock while they still can, as I suspect this is just the beginning of a very promising growth story.

Near-faultless execution has led Tesla Motors to the brink of success, but the road ahead remains a hard one. Despite progress, a looming question remains: Will Tesla be able to fend off its big-name competitors? The Motley Fool answers this question and more in our most in-depth Tesla research available for smart investors like you. Thousands have already claimed their own premium ticker coverage, and you can gain instant access to your own by clicking here now.

2 Upcoming Catalysts for Amarin

Biotech Amarin (NASDAQ: AMRN ) has slide more than 20% since launching its hypertriglyceridemia drug Vascepa in January. The company's market value has dropped following months of indecision regarding the drug's exclusivity status and question marks over the drug's launch. As the stock continues to be hotly debated, there are two catalysts in particular that investors should watch. Health-care analyst Max Macaluso discusses each in the following video.

Can Amarin beat the odds?

Small biotech companies usually crash and burn when it comes to launching drugs -- but can Amarin prove the doubters wrong with its new lipid-lowering drug? In our new premium research report, The Motley Fool's top biotech analyst offers an in-depth look at this drugmaker's upcoming opportunities, along with reasons to buy and sell this stock today. To find out more, simply click here now to claim your copy.

Editor's Note: At 1:00, the speaker meant to say eight months.

The 2 Scariest Market Events This Week

Stocks lost ground on Friday, with the S&P 500 (SNPINDEX: ^GSPC ) down 0.2%, while the narrower, price-weighted Dow Jones Industrial Average (DJINDICES: ^DJI ) gained 0.1%. Still, with a very respectable 1.7% weekly gain, the S&P 500 managed to claw back most of last week's losses.

Mirroring yesterday's one hundredth of a point gain, the VIX Index (VOLATILITYINDICES: ^VIX ) , Wall Street's fear gauge, fell one hundredth of a point today to close at 13.61. (The VIX is calculated from S&P 500 option prices and reflects investor expectations for stock market volatility over the coming 30 days.)

When market machinery breaks down

On Tuesday, at approximately 1:07 p.m. EDT, the following 12-word tweet from the Associated Press's Twitter feed roiled U.S. equity markets:

Breaking: Two Explosions in the White House and Barack Obama is Injured.

The report, which was fake (the AP Twitter account had been hacked), was quickly removed by the AP and denied by the White House. The effect on stocks was a brief 1% decline that was erased in the space of minutes. Nevertheless, the downward spike in the intraday graph illustrates that, in the moment, the episode must have been unsettling for market participants:

The incident also shows the degree to which Twitter's social networking platform has become a key component of the information infrastructure that drives financial market activity. I can attest from personal experience that breaking stories break on Twitter much before they are reported by traditional media outlets.

Two days later, a software problem halted options trading on the Chicago Board Options Exchange, or CBOE, the U.S.'s largest options exchange and part of the CME Group (NASDAQ: CME ) for more than three hours. That was no way to celebrate today's 40th anniversary of the CBOE's first trading day; on April 26, 1973, 911 contracts changed hands, with call options available on 16 U.S. stocks. Beyond individual stocks, the outage meant options on two key indexes, the S&P 500 and the VIX Index, were unavailable.

In the wake of the 2010 "Flash Crash" and last-year's near-failure of Knight Capital due to a rogue algorithm, market participants are much more sensitive to these types of events; but should they have investors concerned? Not really -- not as long as they are truly investors, i.e. they have a multi-year time horizon. For traders, on the other hand, price spikes and unavailability can be very costly. Still, even fundamental investors may want to review my Best Practices for Investors in a Microsecond Market; it pays to be prepared.

If you're ready to invest based on fundamentals and long-term value creation, The Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock it is in the brand-new free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

Saturday, April 27, 2013

Today's 3 Worst Stocks

Friday saw the S&P 500 Index (SNPINDEX: ^GSPC ) break its five-day streak of gains, as investors yawned at the GDP numbers released by the Commerce Department today. Not only was the 2.5% growth rate in the first quarter underwhelming and below most expectations, but corporate earnings also failed to spark much optimism, and the S&P lost 2 points, or 0.2%, to close at 1,582 Friday. A few notable laggards led the way lower.

Only on Wall Street can a company like Amazon.com (NASDAQ: AMZN ) beat expectations, only to see its shares crater 7.2% afterwards. The bearish tone came on fears that the online retail giant's slowing sales growth spells a not-so-rosy future. The trend is hard to deny: Sales rose 22% in the most recent period, compared with a 34% surge in the same period a year ago.

With shares in semiconductor companies among some of the day's biggest losers, KLA-Tencor (NASDAQ: KLAC ) fit right in, slipping 6.8%. If there's one thing investors hate more than falling sales, it's a mix of falling sales and declining profits, a double-whammy of negativity that shareholders clearly weren't expecting Friday. Several analysts lowered their price estimates on the shares following the earnings report, which certainly didn't help the stock's performance.

Quarterly results, or a lack thereof, were also the Achilles' heel of Eastman Chemical (NYSE: EMN ) , which shed 5.1% today. Earnings actually came in above expectations, but sales numbers just didn't cut it, even though the company reported higher revenue in every single geographic region it reports in. Asia especially stood out as a segment of rapid growth, with those sales rocketing more than 50% higher. Although 48% sales growth in Europe, the Middle East, and Africa isn't too shabby, either, especially considering the macroeconomic worries and political instability surrounding those parts of the world.

Everyone knows Amazon is the king of the retail world right now, but at its sky-high valuation, most investors are worried it's the company's share price that will get knocked down instead of its competitors'. The Motley Fool's premium report will tell you what's driving the company's growth, and fill you in on reasons to buy and reasons to sell Amazon. The report also has you covered with a full year of free analyst updates to keep you informed as the company's story changes, so click here now to read more.

The Gory Details on Molex's Double Fumble

Molex (Nasdaq: MOLX ) reported earnings on April 23. Here are the numbers you need to know.

The 10-second takeaway

For the quarter ended March 31 (Q3), Molex missed estimates on revenues and missed estimates on earnings per share.

Compared to the prior-year quarter, revenue grew slightly. Non-GAAP earnings per share dropped. GAAP earnings per share contracted significantly.

Margins contracted across the board.

Revenue details

Molex reported revenue of $852.9 million. The 12 analysts polled by S&P Capital IQ expected a top line of $917.3 million on the same basis. GAAP reported sales were the same as the prior-year quarter's.

Source: S&P Capital IQ. Quarterly periods. Dollar amounts in millions. Non-GAAP figures may vary to maintain comparability with estimates.

EPS details

EPS came in at $0.33. The 14 earnings estimates compiled by S&P Capital IQ anticipated $0.35 per share. Non-GAAP EPS of $0.33 for Q3 were 2.9% lower than the prior-year quarter's $0.34 per share. GAAP EPS of $0.25 for Q3 were 31% lower than the prior-year quarter's $0.36 per share.

Source: S&P Capital IQ. Quarterly periods. Non-GAAP figures may vary to maintain comparability with estimates.

Margin details

For the quarter, gross margin was 29.1%, 140 basis points worse than the prior-year quarter. Operating margin was 9.5%, 140 basis points worse than the prior-year quarter. Net margin was 5.2%, 260 basis points worse than the prior-year quarter. (Margins calculated in GAAP terms.)

Looking ahead

Next quarter's average estimate for revenue is $884.4 million. On the bottom line, the average EPS estimate is $0.36.

Next year's average estimate for revenue is $3.62 billion. The average EPS estimate is $1.48.

Investor sentiment

The stock has a four-star rating (out of five) at Motley Fool CAPS, with 132 members out of 147 rating the stock outperform, and 15 members rating it underperform. Among 44 CAPS All-Star picks (recommendations by the highest-ranked CAPS members), 41 give Molex a green thumbs-up, and three give it a red thumbs-down.

Of Wall Street recommendations tracked by S&P Capital IQ, the average opinion on Molex is hold, with an average price target of $27.95.

Can your portfolio provide you with enough income to last through retirement? You'll need more than Molex. Learn how to maximize your investment income and "Secure Your Future With 9 Rock-Solid Dividend Stocks." Click here for instant access to this free report.

Add Molex to My Watchlist.3 Areas You Must Watch at AIG

In this video, Matt Koppenheffer outlines three things AIG investors need to watch:

The new CEO. Current chief Robert Benmosche came out of retirement to lead AIG out of its financial crisis and performed admirably well. Who will take over the reins? Historically low interest rates that have made life difficult for banks and insurance companies, particularly insurance companies like AIG that underwrite life insurance. The performance of AIG's core businesses. Now that AIG has restructured itself, have its property/casualty and life insurance businesses delivered positive results?Check out the video for more details.

At the end of last year, AIG was the favorite stock among hedge fund managers. Have they identified the next big multibagger, or are the risks facing the insurance giant still too great? In The Motley Fool's premium report on AIG, financials bureau chief Matt Koppenheffer breaks down the key issues that you need to know about if you want to successfully invest in this stock. Simply click here now to claim your copy, and you'll also receive a full year of key updates and expert analysis as news continues to develop.

Why Cabela's Shares Shot Higher

Although we don't believe in timing the market or panicking over market movements, we do like to keep an eye on big changes -- just in case they're material to our investing thesis.

What: Cabela's (NYSE: CAB ) shot perfect once again this quarter, as shares jumped as much as 18% after another strong report.

So what: The sportsmen's outfitter topped earnings estimates by $0.11 a share, posting $0.70 for the period, and revenue jumped a whopping 28.7% to $802.5 million, 4% better that expert's prediction. The vast majority of additional revenue came from same-store sales, which shot up 24%. Management said the growth was driven by expected increases in firearms and ammunition sales, as well as soft goods, footwear, optics, and archery.

Now what: Without firearms and ammunition, same-stores sales increased just 9% -- still strong, but clearly much of Cabela's growth was driven by gun buyers. With the gun hysteria following the Sandy Hook shootings likely to fade now that the Senate has failed to pass any sort of gun control, investors may expect that growth to slow. As the stock has now tripled in the past year and a half, investors may want to take a cue from their senators and sell while the stock is hot.

Don't miss the next update on Cabela's. Add the stock to your Watchlist by clicking right here.

More Expert Advice from The Motley Fool

The Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock in our brand-new free report: "The Motley Fool's Top Stock for 2013." I invite you to take a copy, free for a limited time. Just click here to access the report and find out the name of this under-the-radar company.

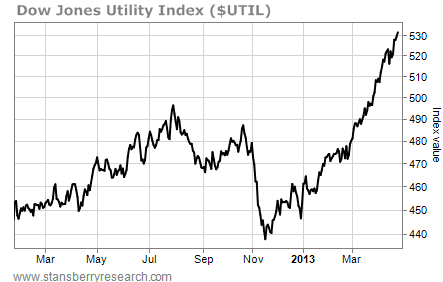

These Four Sectors Look Ripe for a Pullback

Historically, the period between May and November is weak for the stock market. You've probably heard Wall Street advise investors to "sell in May and go away."

Here's a look at a few sectors you may want to "go away" from...

.png)

.png)

.png)

Parabolic moves always end badly. They get overstretched to the upside and then suddenly turn lower. The resulting decline usually wipes out at least 50% (or more) of the move higher. So while utility stocks aren't showing the cautionary weakness of the other sectors, they're still vulnerable to a swift move lower.

– Jeff Clark

Friday, April 26, 2013

The 2 Scariest Market Events This Week

Stocks lost ground on Friday, with the S&P 500 (SNPINDEX: ^GSPC ) down 0.2%, while the narrower, price-weighted Dow Jones Industrial Average (DJINDICES: ^DJI ) gained 0.1%. Still, with a very respectable 1.7% weekly gain, the S&P 500 managed to claw back most of last week's losses.

Mirroring yesterday's one hundredth of a point gain, the VIX Index (VOLATILITYINDICES: ^VIX ) , Wall Street's fear gauge, fell one hundredth of a point today to close at 13.61. (The VIX is calculated from S&P 500 option prices and reflects investor expectations for stock market volatility over the coming 30 days.)

When market machinery breaks down

On Tuesday, at approximately 1:07 p.m. EDT, the following 12-word tweet from the Associated Press's Twitter feed roiled U.S. equity markets:

Breaking: Two Explosions in the White House and Barack Obama is Injured.

The report, which was fake (the AP Twitter account had been hacked), was quickly removed by the AP and denied by the White House. The effect on stocks was a brief 1% decline that was erased in the space of minutes. Nevertheless, the downward spike in the intraday graph illustrates that, in the moment, the episode must have been unsettling for market participants:

The incident also shows the degree to which Twitter's social networking platform has become a key component of the information infrastructure that drives financial market activity. I can attest from personal experience that breaking stories break on Twitter much before they are reported by traditional media outlets.

Two days later, a software problem halted options trading on the Chicago Board Options Exchange, or CBOE, the U.S.'s largest options exchange and part of the CME Group (NASDAQ: CME ) for more than three hours. That was no way to celebrate today's 40th anniversary of the CBOE's first trading day; on April 26, 1973, 911 contracts changed hands, with call options available on 16 U.S. stocks. Beyond individual stocks, the outage meant options on two key indexes, the S&P 500 and the VIX Index, were unavailable.

In the wake of the 2010 "Flash Crash" and last-year's near-failure of Knight Capital due to a rogue algorithm, market participants are much more sensitive to these types of events; but should they have investors concerned? Not really -- not as long as they are truly investors, i.e. they have a multi-year time horizon. For traders, on the other hand, price spikes and unavailability can be very costly. Still, even fundamental investors may want to review my Best Practices for Investors in a Microsecond Market; it pays to be prepared.

If you're ready to invest based on fundamentals and long-term value creation, The Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock it is in the brand-new free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

Telenav Beats on Both Top and Bottom Lines

Telenav (Nasdaq: TNAV ) reported earnings on April 25. Here are the numbers you need to know.

The 10-second takeaway

For the quarter ended March 31 (Q3), Telenav beat expectations on revenues and beat expectations on earnings per share.

Compared to the prior-year quarter, revenue dropped. GAAP earnings per share dropped significantly.

Margins dropped across the board.

Revenue details

Telenav logged revenue of $55.0 million. The four analysts polled by S&P Capital IQ expected net sales of $52.7 million on the same basis. GAAP reported sales were the same as the prior-year quarter's.

Source: S&P Capital IQ. Quarterly periods. Dollar amounts in millions. Non-GAAP figures may vary to maintain comparability with estimates.

EPS details

EPS came in at $0.09. The two earnings estimates compiled by S&P Capital IQ anticipated $0.02 per share. GAAP EPS of $0.09 for Q3 were 47% lower than the prior-year quarter's $0.17 per share.

Source: S&P Capital IQ. Quarterly periods. Non-GAAP figures may vary to maintain comparability with estimates.

Margin details

For the quarter, gross margin was 60.6%, much worse than the prior-year quarter. Operating margin was 7.4%, much worse than the prior-year quarter. Net margin was 7.0%, 570 basis points worse than the prior-year quarter. (Margins calculated in GAAP terms.)

Looking ahead

Next quarter's average estimate for revenue is $43.9 million. On the bottom line, the average EPS estimate is $0.05.

Next year's average estimate for revenue is $192.4 million. The average EPS estimate is $0.14.

Investor sentiment

The stock has a four-star rating (out of five) at Motley Fool CAPS, with 110 members out of 115 rating the stock outperform, and five members rating it underperform. Among 21 CAPS All-Star picks (recommendations by the highest-ranked CAPS members), 20 give Telenav a green thumbs-up, and one give it a red thumbs-down.

Of Wall Street recommendations tracked by S&P Capital IQ, the average opinion on Telenav is outperform, with an average price target of $7.45.

Software and computerized services are being consumed in radically different ways, on new and increasingly mobile devices. Many old leaders will be left behind. Whether or not Telenav makes the coming cut, you should check out the company that Motley Fool analysts expect to lead the pack in "The Next Trillion-dollar Revolution." Click here for instant access to this free report.

Add Telenav to My Watchlist.AT&T Launches Home Technology Management Service

AT&T (NYSE: T ) launched its new home technology management and security service, called Digital Life, in 15 cities across America today.

The company said in press release that users can remotely adjust their house's temperature, check in on their kids, unlock doors, and check if they closed their garage door using the Digital Life system. At the core of Digital Life is the 24/7 professional home monitoring service, which will respond to emergencies and call police.

Digital Life users can control many aspects of their home using their smartphone, tablet, or PC. Users can choose options like indoor and outdoor cameras, remote appliance and thermostat controls, door lock and unlock features, water detection and more. AT&T said in the release that, "People rely on their mobile devices more than ever, so Digital Life offers an easy and convenient way to secure their homes, protect their families and simplify their lives from virtually anywhere."

The new service is currently available in Atlanta, Austin, Boulder, Chicago, Dallas, Denver, Houston, Los Angeles, Miami, Philadelphia, Riverside (Calif.), San Francisco, Seattle, St. Louis, and select areas in the New York and New Jersey metropolitan area. AT&T said Digital Life will expand into 50 additional markets by the end of this year. Pricing for the service starts at around $30 per month, with a $150 installation fee.

How to Find Cash Cows

Long-term investors are often searching for excellent businesses that generate plenty of cash. But how do you find these cash cows? In the video below, Fool contributor Daniel Sparks suggests investors use the ratio of free cash flow to sales. The ratio shows what percentage of every dollar of sales ultimately ends up as free cash flow -- the cash companies can use to pay out dividends, buy back shares, or save for future acquisitions at some point when they make strategic sense.

To illustrate, Daniel compares Apple (NASDAQ: AAPL ) , Google (NASDAQ: GOOG ) , Baidu (NASDAQ: BIDU ) , IBM (NYSE: IBM ) , and Nokia (NYSE: NOK ) .

It's incredible to think just how much of our digital and technological lives are almost entirely shaped and molded by just a handful of companies. Find out "Who Will Win the War Between the 5 Biggest Tech Stocks?" in The Motley Fool's latest free report, which details the knock-down, drag-out battle being waged by the five kings of tech. Click here to keep reading.

Thursday, April 25, 2013

3 Reasons Tesla Stock Will Hit a New High in 2013

Tesla Motors (NASDAQ: TSLA ) continues to prove its critics wrong, one milestone after another. Last year, the company delivered its all-electric Model S ahead of schedule, won Motor Trend's 2013 Car of the Year, ramped up production, and launched a U.S. Supercharger Network. Tesla rode this momentum into 2013, and now expects to post its first profit when the company reports earnings on May 8. Tesla stock is up more than 50% year to date because of all the upbeat news. However, with Tesla's stock trading around $50 a share, some investors worry that it's too late to get in on the action.

Here are three reasons why Tesla stock should move higher from here.

1. Tesla is a disruptive force in the auto industry

Tesla Motors is a disruptive innovator that's bent on forever changing not only the way we drive, but also the way we buy cars. Unlike traditional car manufacturers, such as Ford or General Motors, Tesla doesn't sell its cars through franchised dealerships. Instead, the company's retail strategy relies on mall stores located in high foot-traffic areas.

Not surprisingly, pushing for change in an industry that's operated the same way for more than 100 years hasn't been easy for Tesla. Auto-dealer groups in states such as New York and Massachusetts brought lawsuits against Tesla, saying that it violated state franchise laws. Tesla fought back, and won.

As it stands, Tesla has won the right to operate its manufacturer-owned stores in more than eight U.S. states. Tesla stock should get a meaningful boost if the company can win over the state of Texas in the coming months.

2. The stock's current valuation is deceiving

There's no shortage of investors betting against the company. In fact, as of this writing, Tesla stock has a short interest of more than 42%. For comparison, less than 2% of Ford's stock is currently sold short. Meanwhile, even GM's short float of 12% looks good next to Tesla stock. Nevertheless, this could end up working to Tesla's advantage in the case of a short squeeze.

Additionally, many would-be Tesla investors argue that the stock is overvalued compared to other automakers, such as Ford or General Motors. This isn't without merit if you're simply looking at the numbers. However, as an upstart growth stock, I'd be worried if Tesla's valuation were comparable to these traditional auto companies.

It's a mistake to value Tesla using the short-term benchmarks reserved for established auto companies. Conversely, investors who are willing to take a long-term approach to valuing Tesla stock will have the most to gain when the naysayers buy in down the road -- particularly, if Musk delivers on his promise of making Tesla the greatest automaker of the 21st century.

The lesson here is: Don't judge a stock by its valuation alone. Finding winning investments is about more than numbers. It is equally important to understand the business behind those numbers. In Tesla's case, I think it is one of the most misunderstood stocks on the Nasdaq. However, this will change in time as the company continues to exceed expectations, and that's when longtime shareholders will be rewarded.

3. Visionary leadership at its best

Thanks to Apple's Steve Jobs, the world has seen what visionary leadership can do for a company. Tesla's CEO Elon Musk is no exception. Musk has a proven track record of success, including co-founding PayPal, which, in 2002, was purchased by eBay for a cool $1.5 billion. More recently, Musk made history when his company SpaceX launched the first commercial spacecraft to reach the International Space Station. Not to mention, SpaceX locked down a $1.6 billion contract with NASA, in the process.

While transforming U.S. space travel is certainly remarkable, what Musk has achieved with Tesla is equally impressive. With Musk at the helm, Tesla has overcome insurmountable odds as a start-up electric car company trying to succeed in an industry where economies of scale favor the traditional automakers. If history is any indication, Musk knows how to build and run a successful business.

It isn't everyday that you find CEOs, such as Jobs or Musk, with the vision to revolutionize entire industries. For this reason, I plan to own Tesla stock well into the future, and certainly for as long as Musk remains at the top. Patient investors should buy Tesla stock while they still can, as I suspect this is just the beginning of a very promising growth story.

Near-faultless execution has led Tesla Motors to the brink of success, but the road ahead remains a hard one. Despite progress, a looming question remains: Will Tesla be able to fend off its big-name competitors? The Motley Fool answers this question and more in our most in-depth Tesla research available for smart investors like you. Thousands have already claimed their own premium ticker coverage, and you can gain instant access to your own by clicking here now.

Bears Are Clearing Out of China

Chinese Internet companies aren't racing back into fashion, but naysayers are starting to clear out of the world's most populous nation.

The market exchanges are out with their latest tallies on short sales, and the number of bearish wagers as of mid-April have been falling sharply for many of the country's bellwethers.

There were just 2.2 million shares of Dangdang (NYSE: DANG ) sold short. That's a 52-week low for the Chinese e-tailer, and well below the 9.6 million shares that were sold short in May of last year. SINA (NASDAQ: SINA ) also clocked in with a new low. There were just 1.8 million shares in bearish wagers against the online portal behind the Twitter-like SINA Weibo platform. There were 9 million shares sold short 10 months ago. Renren (NYSE: RENN ) came in at 3.8 million shares sold short, near its low of 3.1 million just two weeks earlier. There were 24.9 million shares of Renren borrowed by skeptics of the leading social networking website operator in May of last year.The exodus isn't universal. Youku Tudou (NYSE: YOKU ) had 11.2 million shorted shares as of mid-April. The leading video streaming website hasn't had this many naysayers since late last year.

Then there's Baidu (NASDAQ: BIDU ) . China's largest online search engine had a recent record 12.8 million shares sold short at the end of March. That number dipped to 12 million on April 15, but it's naturally too early to claim that the bears are moving on at Baidu.

However, the general direction or market sentiment is shifting away from shorting Chinese equities. It's a smart move. Yes, China's economy is having its growth hiccups, but these companies for the most part are growing a lot faster than their stateside counterparts.

Outside of SINA, these companies are expected to grow their revenue by at least 28% this year. SINA's 14% projected top-line spurt isn't exactly shabby, either.

The companies aren't perfect. Dangdang, Renren, and Youku Tudou are all presently losing money. Baidu fell short on the bottom line in its latest quarter. However, these are all companies that are clearly growing in popularity judging by the healthy double-digit revenue growth.

You're doing the right thing, bears. You don't want to get in China's way when it does bounce back.

Betting on China

There's plenty of growth still to be had if you buy the right Chinese growth stocks.

It's incredible to think just how much of our digital and technological lives are almost entirely shaped and molded by just a handful of companies. Find out "Who Will Win the War Between the 5 Biggest Tech Stocks?" in The Motley Fool's latest free report, which details the knock-down, drag-out battle being waged by the five kings of tech. Click here to keep reading.

Nutrisystem Names New CFO

Fort Washington, Penn.-based Nutrisystem (NASDAQ: NTRI ) has a new chief financial officer. On Thursday morning, the diet and nutrition company announced it has hired Michael P. Monahan to become its CFO effective May 22.

At first glance, it seems an unusual choice for a food company, since Monahan served as CFO of PetroChoice Holdings, a privately held distributor of industrial, commercial, and automotive lubricants, since 2009. But in fact, he's an old hand at Nutrisystem. From 2006 to 2009, he served as Nutrisystem's vice president of finance.

Welcoming him back to the fold, CEO Dawn Zier said: "We are pleased that Mike has rejoined the company as Chief Financial Officer. He was universally respected during his previous tenure with the company and is a natural fit for us. He knows our business and saw firsthand the innovation and direct consumer response discipline that propelled the company during our growth phase. His perspective and financial expertise will be invaluable as we work to execute our turnaround plan."

Investors appear to agree. Nutrisystem shares are on the upswing this morning in response to the news, rising 2.2% to past $8 a share.

4 Things That Can Go Right for Apple on Tuesday

Apple (NASDAQ: AAPL ) will have plenty to prove as it heads into Tuesday's fiscal second-quarter report. The market isn't holding out for much, but that goes without saying. Shares of the tarnished tech tastemaker haven't traded this low since late 2011.

I went over four things that could go wrong with Apple's quarterly report on Thursday. Now let's turn the tables, reviewing the things that could turn the market's bearish perception around.

1. Earnings can beat expectations -- for a change

It's been an inauspicious start to the Tim Cook era. The company that routinely blew analyst profit targets away with ease while Steve Jobs was running the show has come up short more often than not lately. Apple has missed Wall Street's bottom-line estimates in two of the past three quarters, and three of the past five. Analysts have been lowering their projections in recent weeks, leading the smart money to wager on yet another miss.

Well, what if it doesn't play out that way?

We know that margins are contracting as consumers opt for cheaper Apple devices that the tech giant sells at smaller markups. Consider that Verizon's (NYSE: VZ ) quarterly report on Thursday provided a glimpse of Apple's own quarter. It's great that 4 million of the 7.2 million smartphones Verizon sold were iPhones. Take that, Android! However, half of those 4 million devices were the older iPhone 4 and iPhone 4S smartphones that wireless carriers continue to sell for $100 to $200 less than iPhone 5 handsets.

Apple will earn less than it did a year earlier. All 49 analysts modeling the company see it that way. However, if Apple earns more than the $10.07 a share that Wall Street is currently targeting, it would indicate that margins don't have to be so lean on the cheaper hardware.

2. Revenue growth can beat expectations

With margin deterioration practically a lock, the market will wonder whether Apple can make up the difference in volume. It's not just profit estimates that have come in lower. Wall Street has been shaving down its top-line forecasts, too. Analysts who were initially expecting double-digit top-line growth at Apple are scaling back their numbers in light of unsettling third-party data. The average target now calls for just 8.4% revenue growth.

Ouch!

One of the reasons for the latest wave of downward revisions is that Apple suppliers are smarting. Apple shares took a hit on Wednesday after Cirrus Logic (NASDAQ: CRUS ) warned of a substantial net inventory reserve. Cirrus Logic's announcement revealed that it had too much inventory of a high-volume product. As an Apple supplier, the popular assumption is that Cirrus Logic is talking about Apple. Even though Cirrus Loigic also pointed out that the customer -- nudge, nudge, wink, wink, Apple -- was migrating to a newer Cirrus Logic component, the market began fearing the worst. Apple stuff isn't selling!

Well, Verizon's report shows that at least Apple iPhones are selling briskly. Tablets may be a harder sell, but never underestimate Apple's continuing penetration of the education market. It's no longer just about sales at the retail level. If Apple is able to beat top-line estimates, this would be an even bigger victory than beating on the bottom.

3. Apple can raise its dividend

Payouts aren't the safety nets that investors thought they would be at Apple. The stock is trading much lower than it was just before it initiated its dividend policy a year ago. When Apple shares peaked as the iPhone 5 hit stores, the stock was yielding 1.5%. The dividend hasn't changed, but a cascading stock price has the yield now all the way up to 2.7%.

Isn't that enough? Aren't we near the yield that investors were clamoring for when Apple's stock was peaking?

Investors are smart. A chunky yield isn't going to help if the fundamentals are deteriorating. However, not jacking up its dividend sends a worrisome message. What is Apple saving up for? Its balance sheet is flush with greenery, and even if most of it is locked up overseas, there's more than enough room for an increase.

A pop in payout may not woo as many income investors as the market believes it will, but the very act of doing so would indicate confidence in the company's future cash flow expectations. So, yes, boosting its payout on Tuesday -- 13 months after initiating its quarterly distributions -- should move the stock higher.

4. You can't spell "innovation" without "ovation"

My final bearish point on Thursday was that Apple could disappoint investors clamoring for something new.

Let's be fair here. Apple doesn't announce new products during its quarterly conference calls. It rents out conference centers for that. However, if there has ever been a time for Apple to tease about its future products, it would have to be at a time when the world is ready to write off Apple as it cranks out its quarterly financials on Tuesday afternoon.

Apple doesn't have to explicitly say that it has a smart watch or an HDTV on the way. However, if it's able to point to announcements in the coming months that will expand its product offerings in a material way, investors may think twice before bailing on the fallen tech star.

Tuesday's going to be interesting, to say the least.

Tech-bots duke it out for your investing pleasure

It's incredible to think just how much of our digital and technological lives are almost entirely shaped and molded by just a handful of companies. Find out "Who Will Win the War Between the 5 Biggest Tech Stocks" in The Motley Fool's latest free report, which details the knock-down, drag-out battle being waged among the five kings of tech. Click here to keep reading.

Wednesday, April 24, 2013

Why Juniper Networks Shares Dropped

Although we don't believe in timing the market or panicking over market movements, we do like to keep an eye on big changes -- just in case they're material to our investing thesis.

What: Shares of Juniper Networks (NYSE: JNPR ) have dropped by as much as 10% today after the company reported preliminary earnings with worse-than-expected guidance.

So what: Revenue in the quarter was $1.06 billion, with non-GAAP earnings per share of $0.24. Both results were mostly in line with expectations, and CEO Kevin Johnson said renewed demand from service providers was offset by weaker performance in enterprise sectors, such as federal and financial services.

Now what: Guidance for the coming quarter calls for revenue in the range of $1.07 billion to $1.1 billion, with adjusted earnings per share of $0.22 to $0.26. Analysts were expecting an adjusted profit of $0.27 per share. UBS is keeping a "neutral" rating, saying Juniper isn't firing on all cylinders. Goldman Sachs still thinks the stock is a "sell" in part because of macro headwinds and a weaker competitive position. Lazard Capital is also "neutral" and is waiting for clarity on product adoption.

Interested in more info on Juniper Networks? Add it to your watchlist by clicking here.

Could Budget Cuts Keep Your Flight Grounded This Summer?

The Federal Aviation Administration has been forced to cut its 2013 budget as part of the sequester mechanism implemented to reduce the federal deficit. In order to cut costs, the FAA is furloughing all of its workers for one day every other week through September. The cuts will have a large impact on the capacity of some major hub airports, depending on the time of day and weather conditions. As a result, the FAA has warned airlines and travelers that they could face excessive delays in some cases.

While some members of Congress have complained that the FAA could have saved money elsewhere in its budget, and a number of airlines sued in federal court to block the cuts, these efforts have so far been unsuccessful. The FAA furloughs went into effect this week. Effects were already being felt in Los Angeles and New York by Sunday night and Monday morning. If these cuts remain in place during the busy summer travel season, fliers could face massive delays and some travelers might avoid flying altogether. This could have a significant negative effect on airlines.

Early effects

The first major signs of trouble became visible on Sunday in Los Angeles. With three fewer controllers per day in the tower at Los Angeles International Airport, the airport experienced delays of up to three hours on Sunday night, with some airlines canceling flights to avoid the backups. On Monday morning, the focus shifted to New York, where all three major area airports faced significant delays.

There were also reports on Monday that the Washington, D.C., airspace was overloaded due to the cutback in controllers. Some southbound flights from Newark Airport had to turn back because Washington air traffic control could not accommodate them. Associated Press pointed out that an 8 a.m. US Airways (NYSE: LCC ) Shuttle flight from Washington to New York left the gate on time but had to wait almost two hours to take off, causing it to arrive in New York later than the 8 a.m. Amtrak Acela train.

Risks for the airlines

Airlines face two distinct risks if FAA furloughs remain in place during the summer travel season. First, customers could choose to avoid flying altogether, if they become worried about the likelihood of delays. People could choose to drive or take the train to avoid short flights like the airline shuttles between New York, Boston, and Washington. Vacationers may choose nearby destinations so they can drive rather than dealing with the hassle of flying. This could have a significant impact on airline revenues this summer.

The other danger for airlines is that passengers who do travel will become disgusted by the delays. Airlines already have a hard time keeping customers happy, and cascading delays will only make it harder to deliver acceptable customer service. A further ratcheting up of customer discontent could continue hurt the most-affected airlines for months or even years after the end of FAA furloughs.

United Continental (NYSE: UAL ) and American Airlines (NASDAQOTH: AAMRQ ) could be affected the most. The two carriers were already at the bottom of last year's Airline Quality Rating survey. Furthermore, both airlines have a strategy of building hubs in the top business markets. These cities – such as New York, Chicago, and Los Angeles – tend to have the most crowded airspace. As a result, these carriers are likely to have multiple hubs hit with significant delays on peak travel days, which could snarl operations across their systems. JetBlue Airways (NASDAQ: JBLU ) could also see a disproportionate effect because its main base of operations is at New York's busy JFK Airport.

Foolish conclusion

Investors should not panic yet; it is possible that a few days of delays will force Congress and the FAA to compromise in order to avoid a national air traffic mess. However, political gridlock in the U.S. could lead to a continuation of the status quo, which could anger travelers and hurt profits at a number of major carriers. With most airlines reporting earnings this week, it will be useful for investors to hear what industry executives have to say about the problem and the ways to minimize the effect on customers.

Solid companies selling at depressed prices have consistently helped generations of the world's most successful investors preserve capital, minimize risk, and achieve long-term, market-trampling returns. For one such company, read our free report: "The 1 Remarkable Stock to Own Now." Just click here to get started.

Tuesday, April 23, 2013

Why the Street Should Love Ansys's Earnings

Although business headlines still tout earnings numbers, many investors have moved past net earnings as a measure of a company's economic output. That's because earnings are very often less trustworthy than cash flow, since earnings are more open to manipulation based on dubious judgment calls.

Earnings' unreliability is one of the reasons Foolish investors often flip straight past the income statement to check the cash flow statement. In general, by taking a close look at the cash moving in and out of the business, you can better understand whether the last batch of earnings brought money into the company, or merely disguised a cash gusher with a pretty headline.

Calling all cash flows

When you are trying to buy the market's best stocks, it's worth checking up on your companies' free cash flow once a quarter or so, to see whether it bears any relationship to the net income in the headlines. That's what we do with this series. Today, we're checking in on Ansys (Nasdaq: ANSS ) , whose recent revenue and earnings are plotted below.

Source: S&P Capital IQ. Data is current as of last fully reported fiscal quarter. Dollar values in millions. FCF = free cash flow. FY = fiscal year. TTM = trailing 12 months.

Over the past 12 months, Ansys generated $274.4 million cash while it booked net income of $203.5 million. That means it turned 34.4% of its revenue into FCF. That sounds pretty impressive.

All cash is not equal

Unfortunately, the cash flow statement isn't immune from nonsense, either. That's why it pays to take a close look at the components of cash flow from operations, to make sure that the cash flows are of high quality. What does that mean? To me, it means they need to be real and replicable in the upcoming quarters, rather than being offset by continual cash outflows that don't appear on the income statement (such as major capital expenditures).

For instance, cash flow based on cash net income and adjustments for non-cash income-statement expenses (like depreciation) is generally favorable. An increase in cash flow based on stiffing your suppliers (by increasing accounts payable for the short term) or shortchanging Uncle Sam on taxes will come back to bite investors later. The same goes for decreasing accounts receivable; this is good to see, but it's ordinary in recessionary times, and you can only increase collections so much. Finally, adding stock-based compensation expense back to cash flows is questionable when a company hands out a lot of equity to employees and uses cash in later periods to buy back those shares.

So how does the cash flow at Ansys look? Take a peek at the chart below, which flags questionable cash flow sources with a red bar.

Source: S&P Capital IQ. Data is current as of last fully reported fiscal quarter. Dollar values in millions. TTM = trailing 12 months.

When I say "questionable cash flow sources," I mean items such as changes in taxes payable, tax benefits from stock options, and asset sales, among others. That's not to say that companies booking these as sources of cash flow are weak, or are engaging in any sort of wrongdoing, or that everything that comes up questionable in my graph is automatically bad news. But whenever a company is getting more than, say, 10% of its cash from operations from these dubious sources, investors ought to make sure to refer to the filings and dig in.

With questionable cash flows amounting to only 0.2% of operating cash flow, Ansys's cash flows look clean. Within the questionable cash flow figure plotted in the TTM period above, stock-based compensation and related tax benefits provided the biggest boost, at 6.2% of cash flow from operations. Overall, the biggest drag on FCF came from capital expenditures, which consumed 8.0% of cash from operations.

A Foolish final thought

Most investors don't keep tabs on their companies' cash flow. I think that's a mistake. If you take the time to read past the headlines and crack a filing now and then, you're in a much better position to spot potential trouble early. Better yet, you'll improve your odds of finding the underappreciated home-run stocks that provide the market's best returns.

Software and computerized services are being consumed in radically different ways, on new and increasingly mobile devices. Many old leaders will be left behind. Whether or not Ansys makes the coming cut, you should check out the company that Motley Fool analysts expect to lead the pack in "The Next Trillion-dollar Revolution." Click here for instant access to this free report.

We can help you keep tabs on your companies with My Watchlist, our free, personalized stock tracking service.

Add Ansys to My Watchlist.4 Stocks Making Moves

The following video is from Tuesday's Investor Beat, in which host Chris Hill and analysts Matt Argersinger and Jason Moser dissect the hardest-hitting investing stories of the day.

In this installment, our analysts discuss four stock market movers. Johnson & Johnson (NYSE: JNJ ) climbs on earnings news. J.C. Penney (NYSE: JCP ) taps a credit line and shares rise. And Goldman Sachs (NYSE: GS ) and Target (NYSE: TGT ) slip despite both reporting better-than-expected earnings.

The relevant video segment can be found between 2:24 and 5:05.

During the financial crisis, Goldman Sachs did so well pivoting to avoid the worst of the fallout that it had to downplay its success to duck public ire and conspiracy theories. Today, Goldman is still arguably the powerhouse global financial name, and yet its stock trades at a valuation of less than half what it fetched prior to the crisis. Does this make Goldman one of the best opportunities in the market today? To answer that question, check out The Motley Fool's special report on the bank. In it, Fool banking expert Matt Koppenheffer uncovers the key issues facing Goldman, including three specific areas Goldman investors must watch. To get access to this report, just click here.

Monday, April 22, 2013

Why Dividends Aren't Keeping Up With the Dow

Many investors follow the Dow Jones Industrials (DJINDICES: ^DJI ) not just because of their selection of high-quality blue-chip stocks, but also because of their history of generous payouts to investors. All 30 of the Dow's components pay a dividend, and many of them offer above-average yields with solid histories of growth.

That's why it may come as a big surprise to discover that over the past year, the dividend yield on the Dow has actually fallen. Should dividend investors be worried that the Dow isn't a good place to find strong income-paying stocks anymore?

What's behind the Dow's yield drop?

Admittedly, the decline in the Dow's dividend yield hasn't been all that substantial -- from 2.53% last year to 2.45% this year. But it stands in stark contrast to other major indexes: The yields on the S&P 500 and Nasdaq 100 have both risen, and even the Russell 2000 index of small-cap stocks has seen its dividend yield grow substantially from last year's levels.

Moreover, it's not as if Dow stocks haven't delivered some solid dividend increases lately. Just earlier this week, Procter & Gamble (NYSE: PG ) declared a payout 7% higher than what it paid in the previous quarter, marking its 57th straight annual dividend increase. Back in February, Coca-Cola (NYSE: KO ) came through with an even more aggressive increase of 10% in its quarterly payout, while 3M (NYSE: MMM ) hiked its dividend by 8%. Both companies also have half-century streaks of increasing payouts annually.

The problem -- if you can call it a problem -- is that the total return of the Dow has managed to outpace even these substantial dividend increases. At current levels, the Dow is more than 1,500 points higher than it was at this time last year, representing a gain of almost 12%. That has made it tough for dividend increases to keep up with the Dow's gains. Payout increases of such magnitude aren't unheard of, but in an economic environment that's far from ideal, they've become increasingly rare.

Don't panic over dividends

That the Dow's yield has declined so little in the face of the index's impressive total returns is a testament to the Dow's dividend-paying power. Investors should look forward to further rises in total dividends from Dow stocks well into the future.

3M's dividend growth goes hand in hand with its long history of invention and innovation. Find out whether 3M has what it takes to become a leader in innovative new products once again by reading The Motley Fool's comprehensive new research report on the company. Simply click here now to claim your copy today.

1 Private Company That'll Kill Your Confidence

While China's e-commerce market is set to grow to half a trillion dollars by 2016, that doesn't mean that Amazon (NASDAQ: AMZN ) and Dangdang (NYSE: DANG ) are bound to benefit the most. In the video below, Fool contributor Kevin Chen explains why it's not that simple, and why Alibaba -- the one company foreigners can't invest in -- should scare investors.

As a private Chinese company, Alibaba is the 800-pound gorilla in the room, commanding 20 to 30 times the market share of Amazon and Dangdang. Because of the economics that surround Ailbaba's market dominance, it's perhaps the only company that will really benefit from China's continued e-commerce boom.

And so far, that's remained true. While Groupon (NASDAQ: GRPN ) seemed poised to boost its profits with Chinese growth, Alibaba's own group-buying website, Juhuasuan, may have been one reason Groupon had to close the China door.

Is there a company that can survive Alibaba's full-frontal assault and profit from e-commerce growth?

Well, there may be one in Mecox Lane. To learn more, click on the video below.

Although Amazon may not have a future in China's e-commerce market, it is still-arguably-the king of the U.S. retail world right now. But at its sky-high valuation, most investors are worried it's the company's share price that will get knocked down instead of competitors'. The Motley Fool's premium report will tell you what's driving the company's growth, and fill you in on reasons to buy and reasons to sell Amazon. The report also has you covered with a full year of free analyst updates to keep you informed as the company's story changes. To access it, just click here now.

Sunday, April 21, 2013

3 Dividend Stocks With Room to Run

It isn't just tiny stocks that are delivering exciting investment returns these days. PepsiCo (NYSE: PEP ) , for example, surprised investors last week by turning in sizzling results.

The snack and beverage giant reported a 12% rise in profits on a 4% jump in revenue. Pepsi's food division was the star of the show, booking higher sales and expanded market share. After a healthy bounce on the earnings release Pepsi's stock is now up better than 20% this year -- or twice the market's return.

With that strong performance in mind, lets take a look at a few more dividend stocks that have the potential to trounce the market.

Home products

Procter & Gamble (NYSE: PG ) has been stuck playing defense for more than a year. After a rough period of underperformance, the company turned to cutting costs and has been clawing back the market share it had lost to rivals. But P&G is in the middle of an aggressive push for sales growth, with several new product launches, along with a big marketing campaign to back it all up. The company's stock yields 3% even after a 20% run so far in 2013. And it's valued at just 18 times earnings. Both of those stats beat smaller rival Clorox, which yields 2.9% and has a P/E ratio of 21.

Toys and games

Don't let Hasbro's (NASDAQ: HAS ) 25% rise this year scare you off. Sure, the company turned in a mixed 2012. Sales growth was a big disappointment in the U.S. But profitability also jumped to 15% in that market, versus 12% the year before. Looking ahead, Hasbro is aiming to continue cutting down the vast number of products it sells so that it can focus on developing its blockbuster brands like Play-Doh and My Little Pony. Hasbro currently yields 3.6%, better than Mattel's 3.3%. The company also sports a P/E of 18, making it a relative deal compared to Mattel's 19.

Food and snacks

At a glance, Kraft Foods (NASDAQ: KRFT ) looks like a spanking new company. Its stock just started trading in 2012, after all. But Kraft Foods' stellar portfolio -- including billion-dollar brands like Kraft and Oscar Mayer -- has taken decades to build. Fresh from its spin-off from Mondelez International, Kraft is a pure play on snacks and food in the North American market that has a lot of room to expand there. After a 10% run in the stock so far this year, Kraft is still cheaper than global competitor PepsiCo. And the company's 4% yield makes it one of the highest yielding stocks around.

Foolish bottom line

You don't have to venture into no-name stocks with questionable prospects to get a chance at real capital appreciation. Big, dividend-paying companies can make for exciting investments, too.

Kraft Foods Group is entering a new era after its recent corporate breakup. Its brand power is indisputable and its market share dominates, but Kraft's growth potential is limited and its heavily commoditized categories face massive pressures. In The Motley Fool's premium report on the company, we guide you through everything you need to know about Kraft, including the key opportunities and threats facing the company. To get started, simply click here now.

Google Is Losing Market Share. Does It Matter?

Publishers such as Pandora (NYSE: P ) , Twitter, and Facebook (NASDAQ: FB ) , are quickly gaining market share in mobile display ads. Is Google (NASDAQ: GOOG ) threatened? Fool contributor Daniel Sparks tells Fool.com's Erin Miller in the following video that the development shouldn't negatively affect Google's stock. After explaining why, he tells investors how they should think of this trend and what they should keep an eye on.

As one of the most dominant Internet companies ever, Google has made a habit of driving strong returns for its shareholders. However, like many other Web companies, it's also struggling to adapt to an increasingly mobile world. Despite gaining an enviable lead with its Android operating system, the market isn't sold. That's why it's more important than ever to understand each piece of Google's sprawling empire. In The Motley Fool's new premium research report on Google, we break down the risks and potential rewards for Google investors. Simply click here now to unlock your copy of this invaluable resource.

Saturday, April 20, 2013

Will Abbott Labs Hit New Highs After Earnings?

On Wednesday, Abbott Labs (NYSE: ABT ) will release its latest quarterly results. The key to making smart investment decisions on stocks reporting earnings is to anticipate how they'll do before they announce results, leaving you fully prepared to respond quickly to whatever inevitable surprises arise. That way, you'll be less likely to make an uninformed kneejerk reaction to news that turns out to be exactly the wrong move.

Abbott is only part of what it used to be, with the highly successful AbbVie (NYSE: ABBV ) pharmaceutical giant having traded as an independent company for a full quarter now. Now on its own, Abbott is free to pursue its own path. Let's take an early look at what's been happening with Abbott Labs over the past quarter and what we're likely to see in its quarterly report.

Stats on Abbott Labs

| Analyst EPS Estimate | $0.41 |

| Year-Ago EPS | $1.03* |

| Revenue Estimate | $5.42 billion |

| Year-Ago Revenue | $9.46 billion* |

| Earnings Beats in Past 4 Quarters | 4 |